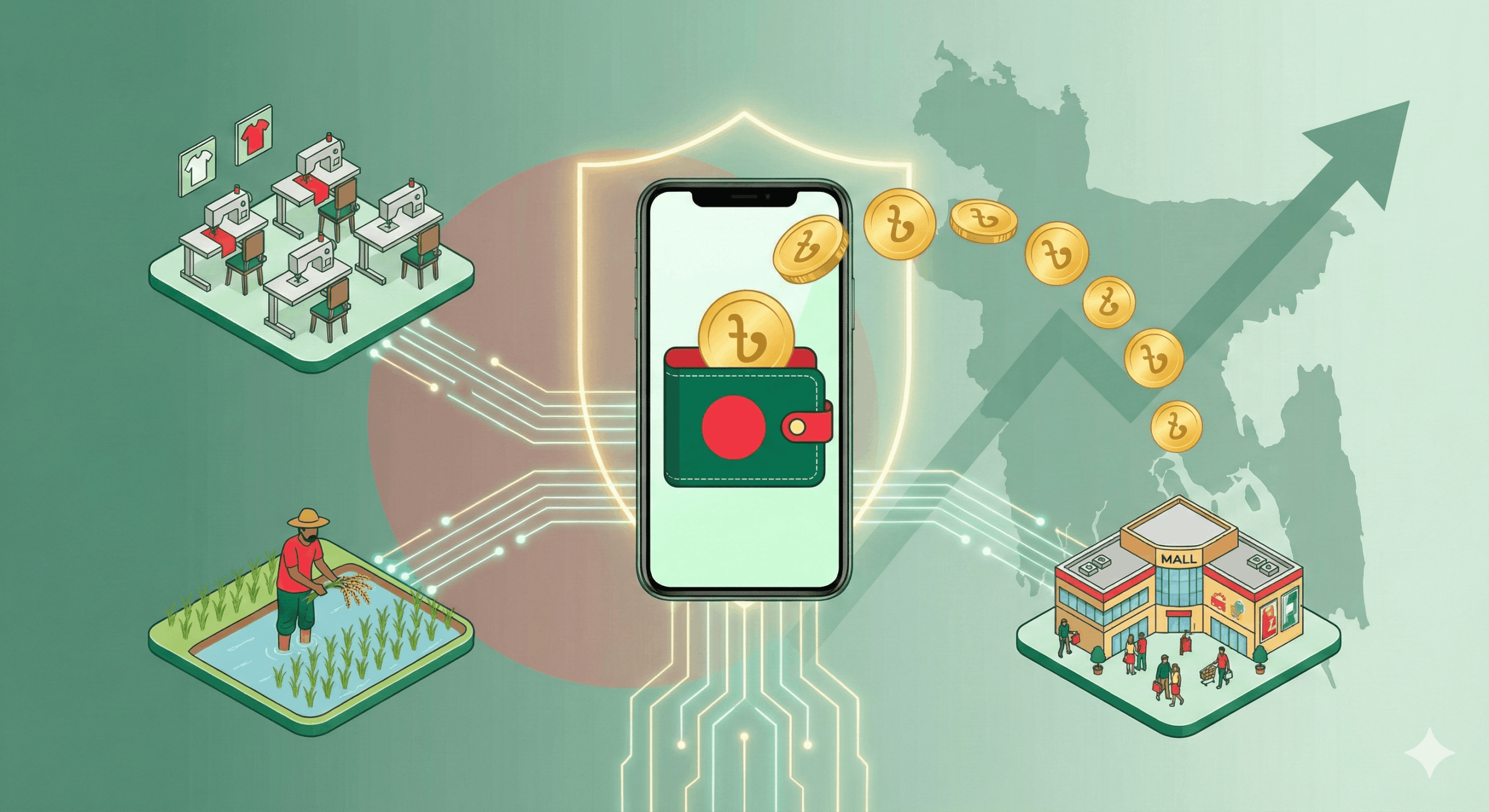

The Cashback Revolution in Bangladesh

Introduction

Remember the days when buying groceries meant fumbling for change or waiting for the shopkeeper to find a 2-taka note? Those days are rapidly fading. Walk into any mudi dokan (grocery shop) or high-end outlet in Dhaka today, and you will likely see a colorful array of QR codes.

The driving force behind this massive shift isn’t just convenience—it’s the allure of Cashback. Mobile Financial Services (MFS) like Bkash, Nagad, Rocket, and Upay have triggered a financial revolution, turning spending into a rewarding experience. In this post, we explore how the cashback culture is reshaping consumer behavior and the digital economy in Bangladesh.

The Rise of MFS Giants

Bangladesh has seen unprecedented growth in digital finance over the last decade. What started as a way to send money home (Send Money) has evolved into a comprehensive lifestyle payment solution (Payment).

-

Bkash: The pioneer that made “Bkash koro” a verb. Their aggressive cashback campaigns on everything from electricity bills to ride-sharing have set the standard.

-

Nagad: Entering the market with lower costs and the “Digital Bank” concept, Nagad shook things up with massive instant cashback offers, especially during festivals like Eid.

-

Rocket & Upay: These players have carved their niches, offering unique rewards for banking integrations and utility payments.

Note: According to Bangladesh Bank data, MFS transactions now account for thousands of crores of Taka daily, a testament to growing trust.

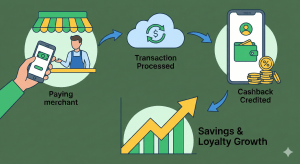

From tea stalls to super shops, QR codes are the new cash registers.

Why “Cashback” is King

Why has this model succeeded so brilliantly in Bangladesh? It taps into a simple consumer psychology: We love value.

-

Instant Gratification: Seeing money return to your wallet immediately after a purchase creates a dopamine hit that physical discounts rarely match.

-

Inflation Hedge: In times of rising prices, getting 5%, 10%, or even 20% back on groceries or clothes feels like a significant win for the middle class.

-

Habit Formation: The campaigns are designed to create habits. Once a user links their bank account or gets used to paying via QR code for a reward, they are less likely to go back to cash.

Beyond Discounts: The Economic Impact

The cashback revolution is about more than just saving a few Taka; it is driving Financial Inclusion.

-

Merchant Adoption: Small merchants who previously dealt only in cash are now part of the digital ecosystem. This builds a credit history for them, potentially opening doors to SME loans.

-

Transparency: Digital transactions reduce the “shadow economy,” bringing more transparency to business turnovers.

-

Less Cash Handling: For both customers and businesses, the risk of theft, counterfeit notes, and the hassle of managing loose change are significantly reduced.

The cycle of savings: Spend digitally, earn instantly.

How to Maximize Your Cashback Earnings

If you want to make the most of this revolution, here are a few pro-tips:

-

Check the Apps Daily: Offers change rapidly. Before ordering food or buying clothes, check the “Offers” section in your Bkash or Nagad app.

-

Look for Partnerships: MFS providers often partner with specific brands (e.g., Bata, Swapno, Daraz) for exclusive “Brand Day” cashback.

-

Use Linked Cards: Some services offer extra cashback if you “Add Money” from a specific bank card before paying.

The Future: Is the Cash-Burn Sustainable?

Critics argue that cashback is a “cash-burn” strategy used to acquire customers. While true, the market is maturing. We are seeing a shift from customer acquisition to customer loyalty. Future rewards might be less about direct cash and more about loyalty points, credit scores, or personalized discounts.

Conclusion

The cashback revolution in Bangladesh is not just a passing trend; it is the bridge to a cashless society. It has taught a nation that has loved cash for centuries to trust the invisible power of digital money. So, the next time you see that QR code, don’t just pay—pay and earn back!